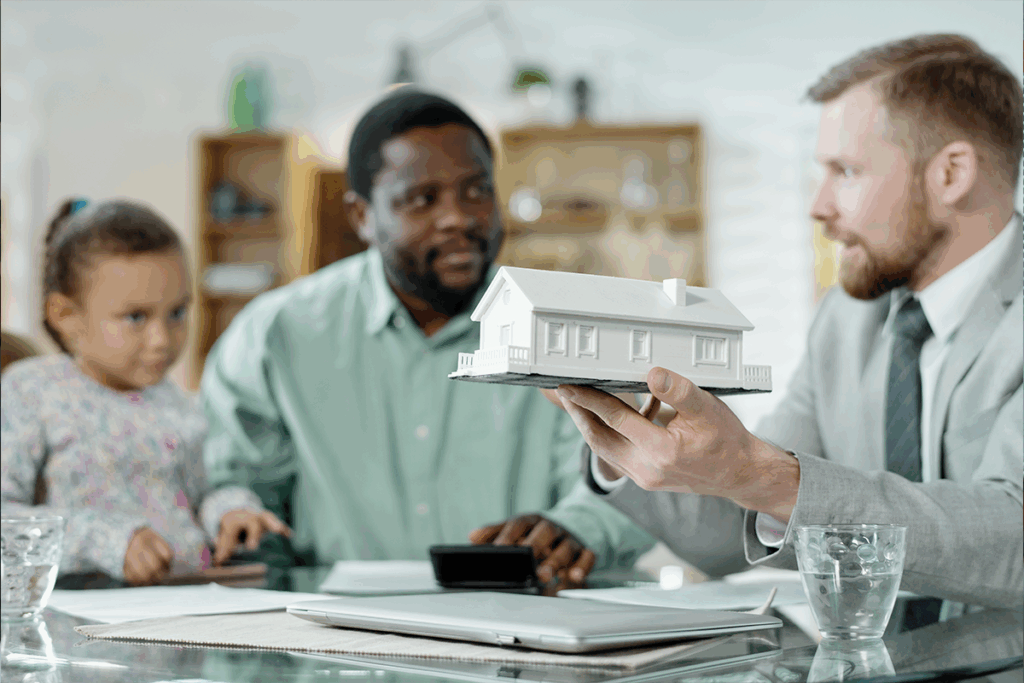

How AI is Transforming Mortgage Lending

Introduction The mortgage lending industry is going through a major transformation. Traditional, manual methods are being replaced by artificial intelligence (AI) technologies that offer faster, more accurate, and more customer-friendly solutions. AI mortgage lending is not just a tech upgrade – it’s changing how banks and lenders help people become homeowners. Lenders today face many challenges, including strict regulations, high operating costs, and the need to meet customer expectations for digital services. Older systems can’t keep up with the number of loan applications or provide accurate risk checks. But AI mortgage lending technologies help lenders turn these challenges into strengths by creating faster and more efficient processes that work better for both lenders and borrowers. 1 – Intelligent Document Processing in Mortgage Lending Handling documents is one of the most time-consuming tasks in mortgage origination. Intelligent document processing mortgage tools now automate this step. These tools use machine learning to quickly identify, extract, and check data from loan documents with high accuracy. Today’s intelligent document processing mortgage systems can handle various documents like W-2s, bank statements, property appraisals, and employment letters. They use optical character recognition (OCR) and natural language processing (NLP) to read and understand content, spot mistakes, and alert lenders about possible compliance issues instantly. By automating data entry and checks, lenders reduce errors and speed up the loan process. These tools can even compare multiple documents and flag mismatches. This gives loan officers more time to focus on helping customers rather than doing repetitive tasks. 2 – AI in Mortgage Application Processing The application stage is often the first direct interaction a borrower has with a lender. AI mortgage application processing improves this experience by quickly reviewing applications, calculating income, and giving instant approval estimates. With AI mortgage application processing, lenders can spot incomplete applications and automatically ask for missing documents. Machine learning algorithms predict the chance of approval, helping loan officers provide better advice early on. This saves time and helps borrowers know where they stand. AI can also pull data from outside sources to verify income, employment, and assets automatically. This makes things easier for borrowers and speeds up verification. Real-time checks mean problems can be fixed immediately, not weeks later. 3 – AI Mortgage Underwriting and Risk Assessment AI is especially powerful in underwriting and risk checks. AI mortgage underwriting tools analyze large amounts of data to assess creditworthiness more accurately than traditional methods. These systems consider many factors at once – like financial history, property details, market trends, and borrower behavior. AI risk assessment mortgage tools go beyond credit scores to give a more complete picture. They also get smarter over time by learning from past loan data. AI mortgage underwriting brings more fairness and consistency by using the same criteria for all applications, reducing human bias. It also creates clear records of how decisions were made, which helps with audits and builds customer trust. AI risk assessment mortgage solutions also adjust to changes in the economy or housing market, allowing lenders to manage risk and pricing more effectively. 4 – AI-Powered Customer Support Great customer service is key to success in lending. AI customer support mortgage solutions are helping lenders deliver faster and better service. Smart chatbots and virtual assistants can answer questions around the clock – like checking application status or explaining needed documents. Advanced AI customer support mortgage tools use natural language processing to understand what borrowers are asking and give tailored answers based on their specific application. AI can also predict when a borrower might run into trouble and notify loan officers to reach out proactively. For example, if a borrower is likely to miss a deadline, the system can schedule a call to help resolve the issue early. 5 – Future Outlook and the Touchless Lending Vision All of these AI innovations are moving the industry toward a “touchless” lending experience. Tavant’s Touchless Lending® Automation platform brings together intelligent document processing, automated underwriting, and AI customer support into a system that can issue clear-to-close decisions in just five days—while cutting costs by up to 77%. This approach is the next step in the evolution of AI mortgage lending. With fewer manual steps, lenders can handle more applications, improve accuracy, and stay compliant. These improvements also allow for more competitive pricing and reaching more borrowers. In the future, we can expect to see even more innovations – like using blockchain for document security, IoT data for property insights, and advanced forecasting tools. These will make mortgage lending even faster, safer, and more reliable. Final Thoughts AI is changing mortgage lending for the better. From intelligent document processing mortgage tools that cut down on manual entry to AI mortgage underwriting and AI risk assessment mortgage tools that improve accuracy and compliance, the benefits are clear. Together with AI mortgage application processing and AI customer support mortgage systems, these technologies are making the loan process smoother, faster, and more transparent for everyone involved. As more lenders adopt AI mortgage lending tools, the industry is moving closer to a future where technology handles the routine work – so lenders and borrowers can focus on achieving homeownership with speed, trust, and confidence. FAQs – Tavant Solutions How is Tavant using AI to transform mortgage lending?AI for property valuation, document processing, predictive underwriting, and risk assessment reduces processing time and improves borrower experience. What specific AI innovations does Tavant bring to mortgage lending?AI property valuations, automated income verification, loan pricing engines, predictive default analytics, NLP for document analysis. How is AI changing the mortgage approval process?Automated underwriting, faster document verification, real-time risk assessment, predictive analytics for loan performance. What are the benefits of AI in mortgage lending?Reduced processing time, lower costs, improved risk accuracy, better customer experience, compliance, higher loan volumes. Can AI completely replace human underwriters in mortgage lending?No, human underwriters are still needed for complex cases and compliance oversight; best approach combines AI and human expertise.

Future Trends in AI Lending: Transforming Financial Services Through Intelligent Automation

The financial services landscape stands at an inflection point. While traditional lending institutions have relied on decades-old processes involving manual underwriting, paper-based documentation, and lengthy approval cycles, artificial intelligence is fundamentally reshaping how lenders evaluate risk, process applications, and deliver capital to borrowers. For C-level executives navigating this transformation, the question isn’t whether AI lending will become mainstream – it’s how quickly your organization can adapt to remain competitive in an increasingly automated marketplace. As borrower expectations shift toward instant gratification and seamless digital experiences, the future of FinTech lending lies in intelligent systems that can process applications, assess creditworthiness, and make lending decisions with minimal human intervention. This evolution toward touchless lending automation represents more than technological advancement; it’s a strategic imperative that will separate market leaders from laggards in the coming decade. Trend 1: Advanced AI Credit Scoring Using Alternative Data Sources Traditional credit scoring models, anchored in historical payment data and limited financial metrics, are giving way to sophisticated AI credit scoring systems that leverage vast arrays of alternative data. Modern machine learning lending platforms now analyze everything from social media behavior and smartphone usage patterns to utility payments and educational credentials to build comprehensive borrower profiles. Alternative data credit scoring represents a paradigm shift in risk assessment methodology. Where conventional models might reject applicants with thin credit files, AI-powered systems can identify creditworthy borrowers by examining non-traditional indicators like consistent rent payments, employment stability patterns, and even digital footprint consistency. This approach not only expands access to credit for underserved populations but also provides lenders with more nuanced risk insights. Leading FinTech companies are already implementing these capabilities. For instance, some lenders now incorporate bank transaction data, subscription payment histories, and even geolocation patterns to supplement traditional credit bureau information. This comprehensive approach to alternative data credit scoring enables more accurate risk prediction while supporting the broader goal of touchless lending automation by reducing manual review requirements. Trend 2: Intelligent Underwriting AI for Real-Time Decision Making The emergence of intelligent underwriting AI is revolutionizing the speed and accuracy of lending decisions. Unlike traditional underwriting processes that require days or weeks for completion, AI-driven systems can analyze complex borrower profiles, assess risk factors, and generate lending recommendations within minutes or even seconds. These intelligent underwriting AI systems excel at pattern recognition across massive datasets, identifying subtle correlations between borrower characteristics and repayment probability that human underwriters might miss. By continuously learning from new loan performance data, these systems become increasingly sophisticated at predicting outcomes and adjusting risk parameters in real-time. The workflow transformation is substantial. Where traditional processes require loan officers to manually review documentation, verify employment, and cross-reference multiple data sources, intelligent underwriting AI can automatically authenticate documents, validate information across databases, and flag potential concerns for human review only when necessary. This shift toward automated decision-making is central to achieving true touchless lending automation while maintaining rigorous risk management standards. Trend 3: Generative AI Integration for Enhanced Customer Experience Generative AI in lending is emerging as a powerful tool for creating personalized borrower experiences and streamlining communication throughout the loan lifecycle. Beyond simple chatbots, advanced generative AI systems can craft customized loan product recommendations, generate personalized financial advice, and even create tailored loan documentation based on individual borrower circumstances. The technology’s ability to process natural language and generate human-like responses makes it particularly valuable for customer service applications. Generative AI in lending can handle complex borrower inquiries, explain loan terms in accessible language, and guide applicants through documentation requirements – all while maintaining consistent messaging and regulatory compliance. Moreover, generative AI can assist loan officers by automatically drafting condition letters, creating summary reports, and generating exception explanations for unusual lending scenarios. This capability not only improves efficiency but also ensures consistency across the organization while supporting the broader vision of AI lending transformation. Trend 4: Predictive Analytics for Proactive Risk Management Machine learning lending platforms are increasingly incorporating predictive analytics to identify potential loan performance issues before they materialize. These systems analyze borrower behavior patterns, economic indicators, and portfolio trends to forecast which loans might become problematic, enabling lenders to take proactive intervention measures. Advanced predictive models can identify early warning signals such as changes in spending patterns, employment instability, or economic stress indicators that correlate with future payment difficulties. This capability allows lenders to reach out to borrowers with assistance programs, modify loan terms, or implement collection strategies before accounts become delinquent. The integration of predictive analytics into AI lending workflows represents a shift from reactive to proactive portfolio management. By identifying risks early, lenders can improve customer outcomes while protecting their own financial interests, creating a more sustainable lending ecosystem. Trend 5: Automated Compliance and Regulatory Monitoring As regulatory requirements become increasingly complex, AI lending systems are incorporating sophisticated compliance monitoring capabilities that automatically track regulatory adherence and flag potential violations. These systems can monitor lending decisions for discriminatory patterns, ensure proper documentation requirements are met, and generate audit trails for regulatory examination. Automated compliance capabilities are particularly crucial as the future of FinTech lending evolves toward more complex AI-driven decision-making processes. Regulators are paying increased attention to algorithmic fairness and explainability, making robust compliance monitoring essential for maintaining regulatory approval and avoiding costly enforcement actions. Risks and Challenges in AI Lending Transformation Despite the tremendous potential of AI lending technologies, organizations must carefully navigate several significant challenges. The risks of AI in lending include algorithmic bias that could result in discriminatory lending practices, model opacity that makes it difficult to explain lending decisions to regulators and borrowers, and over-reliance on automated systems that might miss nuanced risk factors requiring human judgment. Regulatory uncertainty represents another substantial challenge. As AI lending becomes more prevalent, regulatory frameworks are struggling to keep pace with technological advancement. Organizations must balance innovation with compliance, often operating in gray areas where regulatory guidance remains unclear. Data quality and security concerns also pose significant risks. AI lending systems require vast amounts of sensitive financial data, creating cybersecurity vulnerabilities

Benefits of AI-Driven Loan Automation: Transforming the Future of Lending

The lending industry is experiencing a revolutionary transformation as artificial intelligence reshapes how financial institutions process loans, evaluate creditworthiness, and serve customers. Loan automation powered by AI is no longer a futuristic concept – it’s a present-day reality that’s delivering measurable benefits to lenders and borrowers alike. From reducing processing times to improving accuracy and cutting operational costs, AI-driven automation is setting new standards for efficiency and customer satisfaction in the lending landscape. Traditional loan processing has long been plagued by manual workflows, paper-based documentation, and time-consuming approval processes that can take weeks or even months to complete. These outdated systems create frustration for borrowers who expect instant digital experiences and place enormous operational burdens on lenders struggling to compete in today’s fast-paced market. The solution lies in embracing comprehensive loan automation that leverages artificial intelligence to streamline every aspect of the lending process. Modern AI lending platforms are transforming how financial institutions operate, offering unprecedented levels of efficiency, accuracy, and scalability. These platforms integrate seamlessly with existing systems while introducing intelligent automation that can handle complex decision-making processes with remarkable precision. The benefits of implementing AI-driven loan automation extend far beyond simple cost savings, creating value for lenders, borrowers, and the broader financial ecosystem. Accelerated Processing Times and Faster Decisions One of the most immediate and visible benefits of AI loan processing is the dramatic reduction in processing times. Traditional loan applications often require days or weeks to move through various stages of review, documentation, and approval. With intelligent automation, many of these processes can be completed in hours or even minutes, delivering the instant gratification that modern consumers expect. AI loan processing systems can instantly verify income documentation, analyze credit profiles, assess property values, and cross-reference multiple data sources to build comprehensive borrower profiles. This speed doesn’t come at the expense of accuracy – in fact, automated systems often deliver more consistent and reliable results than manual processes. By eliminating the delays associated with manual document review and human processing bottlenecks, lenders can provide borrowers with faster decisions and shorter time-to-close periods. The speed benefits of AI automation extend throughout the entire loan lifecycle. From initial application intake to final approval and funding, AI loan origination software can orchestrate complex workflows that traditionally required multiple handoffs between different departments and systems. This streamlined approach not only improves the borrower experience but also allows lenders to process significantly more applications with the same resources. Enhanced Accuracy Through Automated Underwriting Automated underwriting represents one of the most significant advances in lending technology, replacing subjective human judgment with objective, data-driven analysis. Traditional underwriting processes are susceptible to human error, inconsistent application of guidelines, and unconscious bias that can affect decision quality and regulatory compliance. Automated underwriting systems leverage sophisticated algorithms to analyze vast amounts of data with remarkable precision. These systems can simultaneously evaluate hundreds of risk factors, cross-reference multiple data sources, and apply complex underwriting guidelines consistently across all applications. The result is more accurate risk assessment, better loan quality, and improved portfolio performance for lenders. The accuracy benefits of automated underwriting extend beyond simple risk assessment. These systems can identify patterns and relationships in data that human underwriters might miss, uncovering insights that lead to better decision-making. By removing the variability associated with manual processes, automated underwriting ensures that similar applications receive similar treatment, improving fairness and regulatory compliance. Intelligent Credit Decisioning and Risk Management Automated credit decisioning has revolutionized how lenders evaluate borrower creditworthiness and manage portfolio risk. Traditional credit analysis often relies on limited data points and historical models that may not reflect current market conditions or borrower behavior patterns. AI-powered systems can analyze much broader datasets and adapt to changing conditions in real-time. Automated credit decisioning platforms can process alternative data sources, including banking transaction history, payment patterns, employment history, and even social media activity to build more comprehensive credit profiles. This approach enables lenders to serve borrowers who might not qualify under traditional credit scoring models while maintaining appropriate risk management standards. The risk management benefits of automated credit decisioning are substantial. These systems can continuously monitor portfolio performance, identify emerging risk trends, and adjust decision criteria to maintain optimal risk-return profiles. By leveraging real-time data and adaptive learning capabilities, lenders can make more informed decisions that protect both their interests and their customers’ financial well-being. Machine Learning Capabilities for Continuous Improvement Machine learning underwriting takes automation to the next level by creating systems that improve their performance over time. Unlike traditional rule-based systems that remain static until manually updated, machine learning models can learn from new data, adapt to changing market conditions, and continuously refine their decision-making processes. Machine learning underwriting systems analyze historical loan performance data to identify which factors are most predictive of success or failure. As new loans are originated and performance data becomes available, these systems update their models to reflect new insights and changing patterns. This continuous learning capability ensures that underwriting decisions become more accurate and effective over time. The adaptive nature of machine learning underwriting provides significant competitive advantages for lenders. These systems can quickly identify and respond to changing market conditions, emerging risk factors, and new opportunities for growth. By continuously optimizing their decision-making processes, lenders can maintain strong portfolio performance even as economic conditions and borrower behaviors evolve. Comprehensive AI Loan Origination Software Benefits Modern AI loan origination software provides end-to-end automation that transforms the entire lending process from application to closing. These comprehensive platforms integrate multiple AI capabilities to create seamless workflows that reduce manual intervention while improving accuracy and efficiency. AI loan origination software typically includes intelligent document processing that can automatically classify, extract, and verify information from various document types. This capability eliminates the need for manual data entry while reducing errors and processing delays. The software can also perform automated quality control checks, flagging potential issues before they become problems and ensuring that loans meet all necessary requirements. The integration capabilities of modern AI loan origination software are particularly valuable

Self-Service Loan Applications: A Game Changer

The lending industry is changing forever. Newer technology arrivals and innovative processes are major shifts reshaping customer expectations and industry standards. This is because borrowers expect instant access, digital interactions, and a touchless lending experience. Lenders who fail to meet these demands risk losing relevance in this competitive landscape. Traditional lending workflows are built around manual processes such as branch visits, paperwork, and waiting for loan decisions. If financial institutions are still following such conventional methods, then they simply cannot keep up with modern demands. Among the many innovative solutions introduced in lending, such as AI-based services, the self-service loan application has become a defining transformation in financial services. It allows borrowers to complete the entire application journey independently, while lenders benefit from automation, accuracy, and modern infrastructure. Self-service loan processes are supported by cloud-based loan origination software, digital loan origination solutions, and automation. This makes self-service lending much more than just a convenience; it is redefining what efficiency and customer experience should look like in today’s banking environment. This article further explores self-service loan applications in depth. Let’s get started! What is a Self-Service Loan Application? A self-service loan application is exactly what it sounds like: a way for borrowers to apply for loans without needing constant help from bank staff or loan officers. Instead of scheduling appointments and visiting physical branches, applicants can complete the entire process online, at their own pace, and from anywhere they have internet access. A self-service loan application is basically an end-to-end digital process that makes borrowers independent and allows them to: Start applications online Upload documents digitally Complete verification remotely Receive automated updates Track their application Get faster decisions This is because everything happens through a secure online loan application portal powered by intelligent automation. Such self-service loan applications rely heavily on cloud-based loan origination software and automated solutions. The result is a faster, cleaner, and more efficient loan experience for both borrowers and lenders. How Self-Service Loan Applications Work Self-service lending is a digital process, where you need not physically visit or call banks, financial institutions. The process model integrates automation, compliance, and user experience into a single journey. Here’s how it works: Step 1: Borrower initiates the digital application A mobile-friendly interface guides them through the required details. Step 2: Automated eligibility checks Credit, income, and identity checks run instantly through integrated APIs. Step 3: Document upload with guided prompts Borrowers upload necessary personal information and income documents without emailing or visiting branches. Step 4: Automated loan processing AI and rule-based engines verify data, flag inconsistencies, and assign tasks. Step 5: Underwriting intelligence Risk scoring models evaluate the application based on lender-defined criteria. Step 6: Real-time status tracking Borrowers see each stage eliminating the need for support calls dramatically. Step 7: Instant or near-instant decisioning If approved, loan agreements can be signed digitally. Step 8: Funds disbursal Integrated payment systems allow rapid disbursement. So, this step-by-step process illustrated how self-service loan automation eliminates friction, accelerates turnarounds, and improves borrower satisfaction at scale. The Shift in Borrower Behavior: Why Self-Service Matters Now Digital lending or AI-based lending isn’t just a technological trend; it is a fundamental change that caters to borrowers’ expectations. Why is this shift in the lending journey important for borrowers? Borrowers want speed, not appointments More than 70% of borrowers now prefer lenders who offer fully online journeys. Delays, long forms, and in-person visits immediately increase abandonment rates. Borrowers expect transparency and control This is the cornerstone for users. They want to see application progress in real time. They want clarity on the process, such as documentation, approval status, and decision-making, without even calling customer support. Borrowers judge lenders by digital experience. The current lending market is tech-based, so your brand perception depends on that. Lenders that offer the best services through digitalization gain credibility and trust. Post-pandemic behavior favors self-service. Remote lifestyles and digital banking adoption skyrocketed. So, borrowers now expect 24/7 access and convenience as a standard offering. Such demands and behavioral evolution have made self-service loan applications crucial for loan processing. The Core Benefits of Self-Service Loan Applications for Lenders If you think only borrowers reap benefits from self-service loan applications, think again. The process can transform the internal operations of lending organizations for the better. How? Faster Loan Origination at Scale Self-service loan applications pave the way to a faster origination process with automated systems. This helps lenders reduce manual data entry, document errors, bottlenecks, and repetitive tasks. Moreover, the processing speed of loan applications increases exponentially without additional staff. Reduced Operational Costs Self-service models lower costs by reducing call center workload, eliminating paper processing, minimizing brand dependence, stopping manual intervention, and shrinking verification timelines. Eventually, the productivity of internal teams rises, and cost-per-loan drops. Higher Completion and Conversion Rates Borrowers who can apply anytime complete applications more consistently. A 24/7 digital journey significantly increases conversions. Stronger Compliance and Accuracy Automation enforces standardized workflows, correct document formats, audit trails, and complete form submissions. This ensures that compliance adherence is automated and not done manually. Improved Borrower Experience Borrowers feel in control, informed, and supported, leading to stronger trust and long-term loyalty. What is the Technology behind Today’s Self-Service Loan Applications? Tech stack is key. The technology you adapt to decides how efficient and effective your system truly is. Therefore, modern self-service loan platforms rely on a fully integrated tech stack that includes: Cloud-Based Loan Origination Software This software provides the platforms with scalability, security, and lower operational & maintenance costs. Digital Loan Origination Solutions This automates the entire loan process from application to approval. These solutions typically use AI and machine learning to interact with customers for automated workflows. OCR and Document Intelligence Optical Character Recognition is best for extracting data without manual intervention, and document Intelligence goes a step further by using AI to analyze and understand the context of the documents. API-Driven Integrations They connect different systems such as credit bureaus, banking data sources, and fraud detection systems for loan decision-making.

Reducing Loan Processing Time with AI: A Simpler, Faster Future for Lending

The lending industry is undergoing a complete transformation of processes. It is shifting its operations from traditional methods to modern technology-driven methods. Time and speed are the core changes that have occurred in this digital transformation. Why is that? Well, today borrowers expect fast loan approvals, transparent decisions without bias, and a hands-on, first-class digital experience. As for lenders, they expect efficiency in loan processing time, which cannot be achieved through manual workflows. It’s quite simple, lenders seek solutions to avoid unnecessary risks, customer drop-offs, higher operational costs, and compliance issues. From both perspectives, the expected outcome is saving time and effort. Fintech, as it is, cannot solve the problem of efficiency in the lending industry. This is where AI loan processing comes in. As we know, artificial intelligence is a revolution in this digital era. Similarly, AI is reshaping the entire loan workflow for lenders and creating a seamless experience for borrowers. Ultimately, AI lending reduces processing time from days to minutes by automating repetitive tasks and improving decision accuracy. This article is a guide on how to reduce loan processing time with AI, how AI improves each stage of lending, and how financial services can adapt to scalable, end-to-end loan automation. Why Traditional Loan Processing Takes Too Long Relying on legacy systems and half-baked digital adoption will never lead to reducing loan processing time for lenders. Financial institutions that have adapted to digital systems still face significant delays in the underwriting cycle because traditional glitches continue to exist in the loan processing patterns. What are these glitches? Manual Document Collection & Verification As long as the loan documentation and verification rely on humans, the processing time will be slow. Repetitive Data Entry Financial institutions that depend on manual labor for repetitive tasks, such as borrowers’ data entry, will consume most of the time in the already extended loan processing journey. Human-Driven Underwriting Traditional underwriting requires analysts to evaluate dozens of data points, which leads to inevitable bottlenecks and a time crunch. Departmental Handoffs As each loan application moves between teams for verification, underwriting, quality check, decision-making, etc., the general processing itself is time-consuming. Fraud & Compliance Checks Financial institutions cannot afford to fail in adhering to compliance policies; hence, fraud detection, identity verification, AML checks, and fair lending reviews slow down decision-making. The common factor among all these time-consuming steps is the involvement of human intervention. If a lender relies on teams of manual labor for each step of the workflow, then the increase in loan processing time is inevitable. This would not change, no matter how digital the application front-end looks; the backend processes need automation, and AI has enabled it. What is AI Loan Processing? AI loan processing is the process of using artificial intelligence and automation tools to launch, execute, and complete an entire loan workflow. AI utilizes various tools or procedures to complete said transaction. This includes: Machine learning Optical character recognition (OCR) Natural language processing Predictive analytics Intelligent document processing Automated underwriting models These tools optimize or fully automate tasks across the loan lifecycle by reducing errors, speeding up approvals, and improving risk accuracy. How Does AI Reduce Loan Processing Time? AI lending isn’t about taking over human jobs. AI doesn’t replace human judgment. It simply removes the repetitive manual work so lenders can focus on the most complex, high-risk cases. AI simplifies each phase of the loan workflow. Starting from the initial loan application to final approval, all repetitive tasks can be handled by AI. So, here’s how AI actually reduces loan processing time: 1. AI-Powered Borrower Intake Borrowers’ details are data that act as the deciding factor for loan processing. Borrowers often make mistakes during application submission, such as missing fields, incorrect inputs, unclear document uploads, etc. How AI simplified this stage: Pre-filled forms Smart AI OCRs read the uploaded documents of borrowers, including ID, payroll data, and bank statements, to pre-fill application fields automatically. Real-time error detection AI can find incomplete or inconsistent fields in an application and then flag them. This instantly reverts the application to the borrower and lender, reducing back-and-forth communication and time waste. Personalized guidance AI chatbots help borrowers complete applications, answer questions, and guide documentation. These AI-based loan processing approaches during the initial stage reduce 20-40% in intake delays. 2. Automated Document Collection & Verification Document collection, done manually and then verified, is probably the biggest bottleneck in lending. How AI solves this OCR (Optical Character Recognition) As mentioned earlier, AI uses OCR technology to extract data from borrowers’ IDs, tax returns, bank statements, pay stubs, utility bills, and related loan documents accurately. Document classification AI identifies document types automatically (W-2, 1040, pay stub, bank statement, etc.). Data validation AI cross-checks extracted data with information in the application form. Fraud detection AI detects manipulated documents (altered numbers, edited PDFs, mismatched fonts). This entire process traditionally takes hours or days to get processed. Now, with AI loan processing takes minutes or even seconds. 3. Intelligent Data Aggregation Manual data collection is tiring, time-consuming, and confusing at times. AI eliminates the need for manual data collection. AI pulls information from AI eliminates the need for manual data collection by pulling information from payroll systems, credit bureaus, bank accounts, financial statements, employer databases, public records, and more. AI uses machine learning to map, identify patterns for predictive analysis, and normalize the aggregated data into the lender’s system. Basically, automated aggregation = fewer human errors + faster underwriting. 4. AI Credit Scoring & Automated Underwriting Traditional underwriting is slow and unreliable for proper credit scoring, as it can lead to biased decision-making. Conventionally, analysts must cross-check – credit score, income history, cash flow, employment stability, banking patterns, behavioral data, expenses per month, and risk indicators. Assuming all this is still manually done by teams of employees in your firm, it is safe to say that it is the most tiresome and mentally demanding operation. Thus, with the help of AI, you can speed this up by analyzing hundreds

Personalized Digital Lending is the Future

The lending industry is changing fast. Gone are the days when borrowers had to wait weeks for loan approvals or fill out endless paperwork. Today’s customers want quick, easy, and personalized experiences. They expect their lenders to understand their unique needs and offer solutions that fit their specific situations. This shift is driving the rise of personalized digital lending, which is quickly becoming the new standard in financial services. What is Personalized Digital Lending? Personalized digital lending uses technology to create custom loan experiences for each borrower. Instead of treating all customers the same way, lenders use data and artificial intelligence to understand what each person needs. This means offering the right loan products, at the right time, through the right channels. Think about how Netflix recommends movies based on what you’ve watched before, or how Amazon suggests products you might like. Personalized digital lending works similarly. It looks at a borrower’s financial history, preferences, and behavior to create a lending experience that feels tailor-made just for them. This approach benefits everyone involved. Borrowers get faster approvals, better rates, and a smoother experience. Lenders can reduce costs, minimize risks, and build stronger relationships with their customers. The Current State of Digital Lending The digital lending market has grown tremendously over the past few years. More banks, credit unions, and fintech companies are investing in digital loan origination solutions to stay competitive. These platforms help lenders process applications faster, reduce manual work, and improve customer satisfaction. However, many lenders are still using one-size-fits-all approaches. They might have digital tools, but they’re not using them to create truly personalized experiences. This is where the real opportunity lies. Future of digital lending market trends show that personalization will be the key differentiator between successful lenders and those that fall behind. Why Personalization Matters in Digital Lending Meeting Customer Expectations Today’s borrowers are used to personalized experiences in every part of their lives. They expect their banking and lending experiences to be just as customized. When a lender can offer personalized rates, terms, and communication, it builds trust and loyalty. Improving Approval Rates Personalized lending helps lenders make better decisions about who to approve and what terms to offer. By understanding each borrower’s unique situation, lenders can offer loans to people who might have been rejected under traditional models. This means more approvals and more business for lenders. Reducing Processing Time When lending processes are personalized, they can also be automated. Smart systems can quickly analyze borrower data and make decisions without human intervention. This speeds up the entire process, from application to approval to funding. The Impact of Personalized Lending on Customer Experience The impact of personalized lending on customer experience cannot be overstated. When done right, personalization transforms the entire borrowing journey. Instead of feeling like just another number, borrowers feel understood and valued. Consider a first-time homebuyer versus someone who’s refinancing their third property. These customers have completely different needs, knowledge levels, and concerns. Personalized digital lending recognizes these differences and adjusts accordingly. The first-time buyer might receive educational content and step-by-step guidance, while the experienced borrower gets a streamlined process focused on speed and efficiency. Personalized experiences also extend beyond the application process. Smart systems can send relevant updates, offer additional products when appropriate, and provide ongoing support based on each customer’s preferences and communication style. The impact of personalized lending on customer experience is measurable too. Lenders report higher customer satisfaction scores, increased referrals, and improved retention rates when they implement personalized approaches. Benefits for Different Types of Lenders Banks and Credit Unions Digital lending solutions for credit unions and traditional banks help these institutions compete with fintech startups. Credit unions, in particular, can use personalization to leverage their community focus and member relationships. By understanding their members’ unique needs and financial situations, they can offer more relevant products and services. Digital lending solutions for credit unions often include features like member dashboards, personalized product recommendations, and community-specific loan programs. These tools help credit unions maintain their personal touch while scaling their operations efficiently. Fintech Companies Fintech lenders were early adopters of digital loan origination solutions, but many are now focusing on personalization to differentiate themselves. They can use their technology advantages to create highly customized experiences that traditional lenders struggle to match. Mortgage Lenders The mortgage industry has been particularly active in adopting personalized digital lending. Given the complexity and high stakes of home loans, personalization can significantly improve the borrowing experience while reducing the risk of errors or delays. Challenges in Personalized Digital Lending While the benefits are clear, implementing personalized digital lending isn’t without its difficulties. Understanding these challenges in personalized digital lending helps lenders prepare for a successful transformation. Data Management Personalization requires lots of data, and managing that data can be complex. Lenders need to collect information from multiple sources, ensure it’s accurate and up-to-date, and use it in ways that comply with privacy regulations. This requires robust data management systems and clear policies about how customer information is used. Technology Integration Many lenders use multiple systems for different parts of their operations. Creating a personalized experience often requires integrating these systems so they can share data and work together seamlessly. This can be technically challenging and expensive. Regulatory Compliance The lending industry is heavily regulated, and personalization strategies must comply with fair lending laws and other regulations. Lenders need to ensure that their personalized approaches don’t inadvertently discriminate against certain groups of borrowers. Staff Training Implementing personalized digital lending often requires new skills and processes. Staff members need training on new systems and approaches to customer service. This can be time-consuming and costly, but it’s essential for success. Balancing Automation and Human Touch While automation is important for efficiency, many borrowers still want human interaction for complex decisions like loans. Finding the right balance between automated personalization and human support is one of the key challenges in personalized digital lending. Future Trends in Personalized Digital Lending The future of digital lending market

How AI Reduces Loan Default Risks

The lending industry has always faced one major challenge: predicting which borrowers will pay back their loans and which ones won’t. Traditional methods of assessing loan applications often miss important warning signs, leading to costly defaults that hurt both lenders and borrowers. However, artificial intelligence is changing the game by making loan decisions smarter, faster, and more accurate than ever before. The Problem with Traditional Loan Assessment Before diving into AI solutions, let’s understand why loan defaults happen in the first place. Traditional lending relies heavily on basic credit scores, income verification, and employment history. While these factors are important, they don’t tell the whole story about a borrower’s ability to repay a loan. Human loan officers, no matter how experienced, can only process a limited amount of information at once. They might miss subtle patterns that could indicate future payment problems. Plus, manual review processes are slow and inconsistent, leading to both missed opportunities and poor lending decisions. The result? Higher default rates, increased costs for lenders, and reduced access to credit for deserving borrowers who don’t fit traditional lending criteria. How AI Solutions for Loan Default Reduction Work AI solutions for loan default reduction use advanced algorithms to analyze vast amounts of data in ways that humans simply cannot. These systems can process hundreds of data points simultaneously, identifying patterns and relationships that traditional methods miss. Here’s how AI makes loan decisions smarter: Data Analysis at Scale: AI can examine not just standard financial information, but also alternative data sources like utility payments, rental history, social media behavior, and even shopping patterns. This comprehensive view helps create a more accurate picture of a borrower’s financial responsibility. Pattern Recognition: AI excels at finding hidden patterns in historical loan data. It can identify subtle combinations of factors that historically lead to defaults, even when these patterns aren’t obvious to human analysts. Real-Time Processing: Unlike traditional underwriting that can take days or weeks, AI systems can process loan applications in minutes or even seconds, providing instant risk assessments. Machine Learning for Credit Scoring and Default Risk Machine learning for credit scoring and default risk represents a major leap forward from traditional credit scoring methods. Instead of relying on fixed formulas, machine learning models continuously learn and improve from new data. Traditional credit scores use a limited set of factors and treat all borrowers the same way. Machine learning models, however, can create personalized risk profiles for each borrower. They consider unique circumstances and can adapt to changing economic conditions. For example, a machine learning model might recognize that a borrower with a lower credit score but stable employment in a recession-proof industry actually represents a lower risk than someone with a higher credit score working in a volatile field. These models also get smarter over time. As they process more loan applications and see the outcomes, they refine their predictions and become more accurate at identifying both good and bad risks. Benefits of Using AI for Loan Underwriting The benefits of using AI for loan underwriting extend far beyond just reducing defaults. Here are the key advantages: Improved Accuracy: AI models can achieve default prediction accuracy rates of 80-90%, significantly higher than traditional methods. This means fewer bad loans slip through and fewer good borrowers get rejected unfairly. Faster Decisions: What used to take days or weeks can now happen in minutes. This speed improves customer experience and allows lenders to process more applications efficiently. Reduced Bias: Human decision-making can be influenced by conscious or unconscious biases. AI systems, when properly designed, make decisions based purely on data and statistical relationships, leading to fairer lending practices. Cost Savings: Automated underwriting reduces the need for manual review, cutting operational costs significantly. These savings can be passed on to borrowers in the form of lower interest rates or fees. Better Risk Pricing: AI enables more precise risk assessment, allowing lenders to offer appropriate interest rates based on actual risk levels rather than broad categories. Fraud Detection: AI systems are excellent at spotting inconsistencies and suspicious patterns that might indicate fraudulent applications, protecting lenders from another source of losses. AI in Loan Processing Automation to Reduce Defaults AI in loan processing automation to reduce defaults goes beyond just making approval decisions. It streamlines the entire loan lifecycle to minimize risk at every stage. During the application phase, AI can verify information in real-time, cross-referencing multiple data sources to ensure accuracy. This early verification prevents many problematic loans from moving forward in the process. Throughout the loan lifecycle, AI monitoring systems can track borrower behavior and economic indicators to identify potential problems before they become defaults. For instance, if a borrower’s income drops or spending patterns change dramatically, the system can flag this for early intervention. AI also optimizes loan terms and structures. By analyzing successful loan patterns, AI can recommend optimal loan amounts, terms, and payment schedules that borrowers are most likely to successfully complete. AI Powered Loan Default Risk Assessment Tools Modern AI powered loan default risk assessment tools combine multiple AI technologies to create comprehensive risk management systems. These tools typically include: Predictive Analytics Engines: These analyze historical data to forecast future payment behavior with remarkable accuracy. Natural Language Processing: This technology can analyze text-based information like employment letters, bank statements, and even social media posts to extract relevant risk indicators. Computer Vision: For document verification, AI can automatically read and verify information from pay stubs, tax returns, and other financial documents, ensuring accuracy and detecting potential fraud. Real-Time Monitoring: Once loans are approved, AI systems continuously monitor borrower accounts and external factors that might affect repayment ability. Early Warning Systems: These tools can predict when a borrower might be heading toward financial difficulty, allowing lenders to proactively offer assistance or modify loan terms. The Human Touch in AI-Driven Lending While AI dramatically improves loan decision-making, it doesn’t completely replace human judgment. The best lending systems combine AI’s analytical power with human oversight and empathy. AI handles the heavy lifting of

Enhancing the Borrower Experience with AI: The Future of Lending is Now!

Getting a loan used to be like running an obstacle course. Mountains of paperwork, weeks of waiting and endless phone calls made borrowing money a stressful experience for millions of people. But times are changing. Thanks to artificial intelligence (AI), lenders are finding new ways to make borrowing money smoother, faster and more personal. The Lending Revolution The lending industry is undergoing a massive transformation. Traditional banks and financial institutions are embracing digital lending to stay competitive and meet modern borrower expectations. Today’s customers want the same convenience they get from ordering food or shopping online – quick, easy and 24/7. This demand for better service is forcing lenders to rethink how to improve borrower experience from the ground up. AI is at the heart of this change. It’s not just about replacing humans with machines; it’s about using smart technology to do the routine stuff so humans can focus on what they do best – helping customers make big financial decisions. What’s Special About AI in Lending? Artificial intelligence in lending is like having a super smart assistant that never gets tired, never forgets details and can process thousands of documents in seconds. Unlike traditional computer programs that follow simple rules, AI can learn from patterns, make predictions and even understand natural language. Think of AI as a highly experienced loan officer who has seen millions of applications and remembers every detail. This “digital brain” can spot important information quickly, identify potential problems early and suggest the best loan options for each individual borrower. Key AI Applications That Improve Borrower Experience Smart Document Processing One of the most practical AI use cases in lending is intelligent document processing for loans. Borrowers used to have to gather countless documents – pay stubs, bank statements, tax returns and more – and wait days or weeks for manual review. AI changes this completely. Modern intelligent document processing for loans can read and understand documents instantly, just like a human would, but much faster. These systems can extract key information from a messy bank statement, verify employment details from a pay stub and even detect if documents have been altered. So borrowers get answers in minutes not days.For example, when someone uploads their bank statements, AI can calculate their average monthly income, identify spending patterns and assess their financial stability. This instant analysis helps lenders make faster decisions and reduce errors. Personalized Loan Matching Another great application is personalized loan offers AI. Instead of offering the same loan terms to everyone, AI analyzes each borrower’s unique financial situation to create tailored recommendations. Personalized loan offers AI systems consider factors like income stability, spending habits, debt-to-income ratio and even life circumstances to suggest the best loan products. If someone has excellent credit but irregular income due to freelance work, the AI might recommend a different loan structure than it would for someone with steady employment but average credit. This personalization goes beyond just loan terms. AI can determine the best communication method for each borrower – some prefer text updates, others want phone calls and some like email notifications. The system adapts to individual preferences so the entire experience feels more human and less robotic. Predictive Risk Assessment AI is great at predicting outcomes by analyzing patterns in historical data. In lending, this means better risk assessment for both lenders and borrowers. Instead of relying on credit scores, AI considers hundreds of factors to predict loan performance. This analysis often reveals that some borrowers with lower credit scores are good risks and others with high scores are unexpected challenges. By making more accurate predictions, AI allows lenders to approve more loans and offer better terms to deserving borrowers. The Digital Transformation Impact Digital lending powered by AI delivers many benefits that address common borrower pain points: Speed: What used to take weeks now takes hours or days. AI can process applications, verify information and generate loan decisions much faster than traditional methods. Convenience: Borrowers can apply anytime, anywhere using their smartphones or computers. AI-powered systems work 24/7 so there’s no need to take time off work to visit a bank branch. Transparency: AI provides real-time updates on application status, explains requirements and offers instant feedback on potential issues. Borrowers always know where they are in the process. Accuracy: By reducing human error and automating routine tasks, AI ensures applications are processed correctly the first time, no delays and no frustration. Real-World Implementation: Leading lenders are already seeing great results from AI in lending. Some are reducing loan processing time from 30 days to 3 days. Others are increasing approval rates by 20% while maintaining the same risk standards because AI is identifying borrowers that traditional methods would have missed. One effective approach is to combine multiple AI technologies into a single platform. These systems handle everything from application intake to final loan approval, creating a seamless experience that guides the borrower through each step. For example, when a borrower starts an application, AI can pre-fill forms using public information, suggest missing documents and provide estimated loan terms in real-time. If questions arise, intelligent chatbots provide instant help, while complex issues are automatically routed to human experts. The Human Element While AI does a lot of the heavy lifting, successful digital lending still values human interaction. The goal isn’t to eliminate human contact but to use AI to handle routine tasks so loan officers can focus on guidance, complex questions and building relationships with borrowers. Many borrowers like having access to both AI-powered self-service and human support when needed. This hybrid approach means tech-savvy customers can move quickly through the process while those who prefer personal attention still get the support they need. What’s Next: The Future of AI in Lending The question isn’t if AI will continue to transform the lending industry – it’s how fast and how comprehensive this change will be. Emerging technologies will bring even more sophisticated personalized loan offers AI that considers real-time financial data, social factors and economic